How Private Equity and CPA Firm Buyers Evaluate Quality of Earnings (QoE) in 2026 – Complete Guide

Ashley-Kincaid | July 6, 2026

Selling a CPA firm in 2026 requires far more than strong historical revenue or solid client relationships — it demands strong Quality of Earnings (QoE). For the majority of independent practices in the common $750K–$5M revenue range, this has become the single most important factor determining valuation, deal structure, and ultimate success of the transaction.

In today’s competitive and fragmented CPA M&A market, sophisticated buyers — particularly private equity platforms and experienced strategic acquirers — no longer accept surface-level financials at face value. They conduct a rigorous QoE analysis to understand the true sustainability, predictability, and transferability of the firm’s profits after the sale.

Central to this evaluation is a deep dive into revenue composition: the mix of engagement types (including individual tax returns (1040s), corporate returns (1120/1120S), partnership returns (1065s), non-profit returns (990s), monthly CAS and bookkeeping services, advisory work, audits, and one-time projects), the average fees generated by each service line, client concentration levels, recurring revenue percentage, seasonality patterns, and realization rates. These elements collectively reveal how resilient the firm’s cash flow will be under new ownership and how much risk the buyer is assuming.

Firms with a healthy balance of higher-value, recurring engagements (such as CAS and advisory) and strong average fees typically receive premium treatment. Conversely, practices heavily weighted toward low-fee, seasonal 1040 work or one-time projects often face valuation discounts, extended due diligence, or more conservative offers.

This guide provides the buyer’s framework, realistic examples, calculations, case studies, and a preparation checklist tailored to firms in this segment.

1. Introduction: Why Quality of Earnings Is the Deciding Factor in 2026 CPA Firm Sales

For many CPA firm owners with practices generating between $750K and $5M in annual revenue — the most common segment in today’s highly fragmented CPA market — preparing for sale means navigating an increasingly sophisticated and competitive buyer landscape. Traditional “rule of thumb” revenue multiples (such as 0.9x–1.4x gross revenue) still play a role, particularly for smaller or more owner-dependent firms. However, sophisticated buyers, including private equity platforms and experienced strategic acquirers, are shifting their focus toward a deeper evaluation of Quality of Earnings (QoE) and normalized EBITDA.

These buyers want to understand not just what the firm earned in the past, but how sustainable and transferable those earnings will be under new ownership. They perform detailed due diligence to separate high-quality, recurring profits from one-time events, owner-specific benefits, seasonal spikes, or low-margin work that may not survive the transition. For more on this process, see our pillar guide: How Private Equity and CPA Firm Buyers Evaluate Quality of Earnings (QoE) in 2026.

A modest but well-documented improvement in validated earnings quality — through better revenue mix, stronger average fees, cleaner add-backs, or improved client retention — can meaningfully increase your exit value, sometimes by hundreds of thousands or even millions of dollars. On the other hand, weaknesses in revenue composition, poor documentation of add-backs, or high concentration risk can lead to lower offers, larger escrows, extended due diligence periods, or even lost deals.

This comprehensive guide breaks down exactly what buyers look for when evaluating QoE in CPA firms, with practical insights tailored to firms in the $750K–$5M range.

2. What Is Quality of Earnings (QoE) in CPA Firm M&A?

Quality of Earnings (QoE) is a specialized financial due diligence process that goes well beyond a standard audit. It rigorously assesses whether a CPA firm’s reported earnings are truly sustainable, repeatable, and transferable to a new owner after the sale.

Rather than simply verifying historical compliance with GAAP, a QoE analysis focuses on normalizing the financial statements by identifying and adjusting for non-recurring items, owner-specific expenses, discretionary spending, seasonal fluctuations, and other factors that may inflate or distort current profitability. It also evaluates key risk factors that matter most to buyers — such as revenue mix and quality, client concentration, average fees by engagement type, working capital requirements, operational dependencies, and succession readiness. For more on how buyers evaluate these factors, see our pillar guide: How Private Equity and CPA Firm Buyers Evaluate Quality of Earnings (QoE) in 2026.In essence, QoE helps buyers answer the critical question:

“If we acquire this firm today, what level of reliable, ongoing earnings can we realistically expect in the future?”

3. The Buyer’s 5-Pillar QoE Evaluation Framework

3.1 Revenue Quality Analysis

Buyers treat revenue quality as one of the most important pillars, especially for firms in the $750K–$5M range.

Key Factors Evaluated:

Recurring Revenue Percentage — Ideally moving toward 70% or higher. Buyers strongly prefer predictable, month-to-month or annual recurring revenue (such as CAS, bookkeeping, outsourced CFO, and retainer-based advisory work) over seasonal or one-time projects because it reduces risk and improves cash flow forecasting. See our article on engagement type mix.

Client Concentration — Measured by the percentage of revenue from the top 5 or top 10 clients. Lower concentration (ideally no single client exceeding 15–20%) is viewed favorably, while high concentration raises significant red flags regarding retention risk after the owner departs.

Engagement Type Mix — The balance between different service lines (e.g., 1040s, 1120/1120S, 1065s, 990s, audits, CAS, advisory, and project work). A diversified and higher-value mix is preferred. See our post on engagement type mix and multiples.

Average Fees per Engagement — Higher average fees per client or per engagement typically signal stronger pricing power, better client relationships, and more profitable work. Buyers analyze this by service line to gauge overall revenue quality and margin potential.

Seasonality and Realization Rates — How much revenue is tied to tax season versus year-round services, and how consistently the firm collects billed fees (realization rate).

Client Retention and Tenure — Historical retention rates and average client longevity, which indicate stickiness and transferability of the book of business. See our article on client retention trends.

Engagement Type & Average Fees Impact on Multiples – Realistic View:

| Engagement Type | Typical Average Annual Fee ($750K–$5M Firms) |

QoE Quality Rating | Typical EBITDA Multiple Impact |

|---|---|---|---|

| Monthly CAS / Bookkeeping / Outsourced CFO | $3,600 – $9,500 | Highest | +0.4x to +0.9x |

| Recurring Advisory / Consulting | $5,000 – $14,000 | High | +0.25x to +0.6x |

| Audit / Review Engagements | $7,500 – $22,000 | High (if recurring) | +0.15x to +0.5x |

| Individual Tax Returns (1040s) | $550 – $1,800 | Moderate-Low | Neutral to -0.35x |

| Corporate Tax Returns (1120 / 1120S) | $2,200 – $7,500 | Moderate | Neutral to +0.2x |

| Partnership Tax Returns (1065) | $3,000 – $9,500 | Moderate-High | +0.1x to +0.35x |

| Non-Profit Tax Returns (990s) | $3,500 – $11,000 | Moderate-High | Neutral to +0.25x |

| One-Time / Project Work | Highly variable | Lowest | -0.3x to -0.7x |

How This Affects Multiples Stronger mixes (higher CAS, advisory, 1065s, and 990s with solid average fees) support positive adjustments and higher EBITDA multiples. Heavy 1040 reliance often leads to discounts due to seasonality and lower pricing power.

Example for a $2.8M Firm (typical in this range):

Stronger mix → potential 4.0x–5.0x normalized EBITDA

Heavy 1040 concentration → closer to 3.2x–4.0x

This difference can represent hundreds of thousands (or more) in sale proceeds.

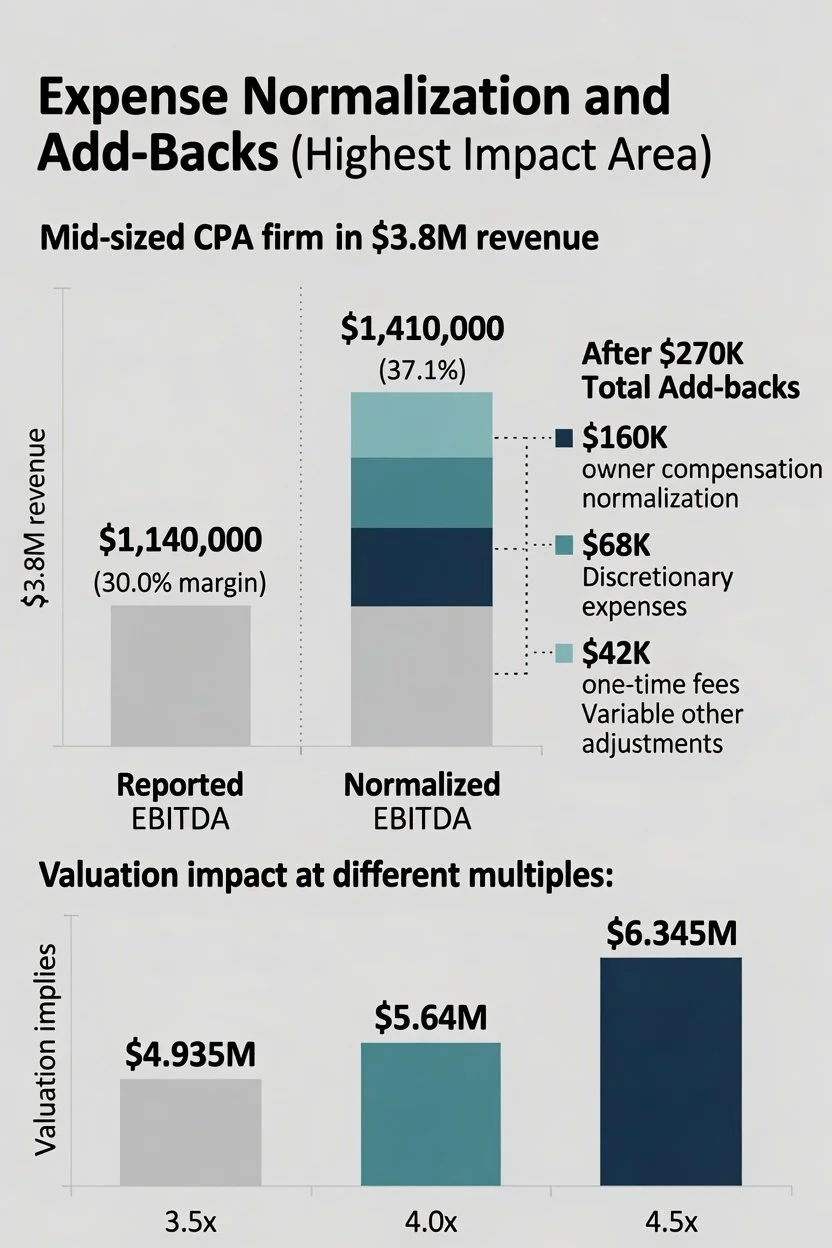

3.2 Expense Normalization and Add-Backs (Highest Impact Area)

This pillar often creates the greatest opportunity for value creation or loss during a sale. Buyers scrutinize expenses to determine what portion of current “profit” is truly sustainable versus owner-specific or non-recurring.

Detailed Sample Calculation – Mid-Sized CPA Firm ($3.8M Revenue, representative of $750K–$5M segment)

Reported Financials:

Revenue: $3,800,000

Reported EBITDA: $1,140,000 (30.0% margin)

Buyer-Accepted Adjustments (examples of commonly allowed add-backs):

Owner compensation normalization: Founding partner takes $420K but a market-rate replacement salary for the role is ~$260K → +$160K add-back

Discretionary expenses (personal vehicles, travel, meals, entertainment, and family-related costs run through the business) → +$68K

One-time legal, consulting, or marketing fees → +$42K

Other common adjustments (e.g., above-market rent to related party, non-recurring repairs, or one-time bonuses) → Variable

Total Add-Backs: +$270K (in this example)

Normalized EBITDA: ~$1,410,000 (37.1% margin)

Valuation Impact (Total Enterprise Value):

At 3.5x multiple → $4.935 million

At 4.0x multiple → $5.64 million

At 4.5x multiple → $6.345 million

This example illustrates how proper normalization and documentation can meaningfully increase the firm’s sale price — often by seven figures. Buyers in the $750K–$5M segment are especially careful with add-backs and will often challenge aggressive or poorly supported ones.

3.3 Working Capital & Balance Sheet Analysis

Working capital is another critical component of the buyer’s Quality of Earnings review. Unlike fixed assets, working capital represents the day-to-day operating liquidity required to run the business. Buyers establish a “normal” working capital peg — a baseline level of net working capital (current assets minus current liabilities) that is expected to remain in the business post-closing.

Why This Matters for CPA Firms CPA practices often experience significant seasonality, particularly around tax season. Revenue and receivables spike in the first half of the year, while expenses (staff bonuses, marketing, software renewals, etc.) may also fluctuate. Buyers analyze historical monthly trends to determine a realistic “peg” that reflects ongoing operational needs rather than temporary peaks or troughs.

How Buyers Calculate the Peg They typically review 12–36 months of balance sheet data and calculate an average or “normalized” level of working capital. Common components include:

Accounts receivable (with attention to aging and collection trends)

Work-in-process (WIP) and unbilled revenue

Prepaid expenses

Accounts payable and accrued liabilities

Deferred revenue

Dollar-for-Dollar Purchase Price Adjustments Any deviation from the agreed working capital peg at closing results in a direct dollar-for-dollar adjustment to the purchase price.

If actual working capital is higher than the peg → Seller receives an additional payment.

If actual working capital is lower than the peg → Buyer receives a reduction in the purchase price.

For $750K–$5M firms, these adjustments can easily range from $50K to several hundred thousand dollars, making accurate forecasting and clean balance sheet management essential.

Best Practice for Sellers Start tracking and normalizing working capital 12–18 months before going to market. Document seasonal patterns clearly and be prepared to explain unusual fluctuations. Firms with consistent collection practices, low bad debt, and well-managed WIP typically fare better in this analysis. For more on how buyers evaluate financials, see our pillar guide on Quality of Earnings.

3.4 Operational, Staffing & Succession Risks

Beyond the numbers, buyers thoroughly evaluate the operational backbone of the firm — especially for $750K–$5M practices where owner involvement is often still significant. They assess how easily the business can continue operating smoothly after the current owner(s) exit.

Key Areas Buyers Scrutinize:

Depth of Management Team Buyers look for a strong second-tier leadership bench. Firms that rely heavily on the owner for day-to-day operations, client relationships, or key decision-making are viewed as higher risk. A well-developed management team (managers, senior accountants, or a COO/CFO equivalent) that can handle operations and client retention post-sale can add 0.3x to 0.6x to the multiple. See our article on succession readiness and transition risk.

Technology Infrastructure Modern, cloud-based systems (practice management software, document management, client portals, automated workflows, and integrated accounting tools) are strongly preferred. Outdated, on-premise, or paper-heavy processes raise concerns about efficiency, scalability, and integration costs for the buyer. Firms with advanced technology often receive positive adjustments, while those with legacy systems may face discounts or longer transition periods. See our post on technology infrastructure as a valuation factor.

Key Person Risk and Client Transition Plans Buyers evaluate how dependent major clients are on the selling owner(s). They review client tenure, relationship strength, and documented transition plans. Firms with formal client succession strategies, strong team-client relationships, and low “owner-only” clients score much better. High key person risk (where many clients would likely leave with the seller) is one of the biggest valuation detractors in this revenue range. See our article on client retention trends.

Overall Impact Weakness in these operational and succession areas can lead to lower multiples, higher escrows, or requirements for longer seller earn-outs or transition periods. Conversely, a firm with a solid team, modern systems, and clear client transition plans signals lower risk and supports stronger offers.

3.5 Accounting Policies & Internal Controls

The final pillar of the buyer’s QoE review focuses on the reliability and consistency of the firm’s accounting practices and internal controls. Buyers want assurance that the financial statements are not only accurate but also prepared in a way that will hold up under new ownership.

Key Areas Evaluated:

Consistency in Revenue Recognition Buyers examine how the firm recognizes revenue across different engagement types (e.g., when is a 1040 considered earned? How is WIP for advisory or CAS work recorded?). Inconsistent or aggressive revenue recognition policies can raise red flags and lead to adjustments during normalization. See our pillar guide on Quality of Earnings.

Accruals and Expense Matching Proper accrual accounting (matching expenses to the periods they relate to) is closely reviewed. Common issues include deferred bonuses, prepaid insurance, or unpaid vendor invoices that distort true profitability.

Financial Reporting Systems and Controls Buyers assess the quality of internal controls, segregation of duties, and the reliability of the firm’s accounting software. Firms using modern, cloud-based systems with good audit trails and automated reconciliations score higher. Manual, error-prone, or outdated processes may lead to additional scrutiny or negative adjustments. See our article on technology infrastructure as a valuation factor.

Overall Financial Discipline Clean books, timely month-end closes, accurate WIP schedules, and consistent accounting policies signal a professional, well-run practice — traits that reduce perceived risk and support higher multiples.

Impact on Valuation Weak accounting policies or poor internal controls can result in larger purchase price adjustments, higher escrow amounts, or even require the seller to provide extended representations and warranties. Strong, consistent financial controls help build buyer confidence and can positively influence the final multiple.

4. Common Red Flags That Reduce Offers or Kill Deals

Even if a CPA firm has solid revenue on paper, certain issues can significantly reduce buyer interest, lower the multiple, increase escrows, or cause the deal to fall apart. Here are the most common red flags buyers look for:

Unsupported or Aggressive Add-Backs Buyers are highly skeptical of large owner compensation add-backs, discretionary expenses, or one-time items without strong documentation. If add-backs appear inflated or lack clear justification (market salary surveys, detailed expense schedules, etc.), buyers will often disallow a large portion, directly reducing normalized EBITDA and the final offer. See our guide on qualitative multiple adjustments.

Declining Client Retention Trends A pattern of client loss, especially among larger or more profitable clients, is a major concern. Buyers review retention rates over the past 3–5 years. Consistent or declining retention signals potential attrition risk after the sale and often leads to lower multiples or higher holdbacks. See our article on client retention trends.

Heavy Owner Dependency Without a Transition Plan If many key clients and day-to-day operations depend primarily on the selling owner(s), buyers see high key-person risk. The absence of a documented client transition plan, trained successors, or strong second-tier team can result in substantial valuation discounts or requirements for longer seller earn-outs and transition periods (often 1–3 years). See our post on succession readiness and transition risk.

Inconsistent Financial Reporting Frequent adjustments to prior financials, late month-end closes, poor WIP tracking, or inconsistent accounting policies raise concerns about reliability. Buyers prefer firms with clean, timely, and consistent financials that can be easily integrated into their systems.

Significant Related-Party Transactions Without Fair Market Value Support Common examples include below-market rent paid to the owner’s real estate entity, family members on payroll at above-market rates, or personal expenses run through the firm. Without proper fair market value documentation or appraisals, buyers will normalize these items downward, reducing the purchase price. See our article on related party transactions.

Additional Red Flags:

High concentration in low-fee seasonal work (e.g., heavy 1040 reliance)

Poor technology infrastructure or manual processes (see our post on technology infrastructure)

Pending litigation, regulatory issues, or compliance problems

Lack of diversification in service offerings or geographic markets

Bottom Line: Identifying and addressing these red flags early (ideally 12–24 months before selling) can protect and even enhance your firm’s valuation.

5. Frequently Asked Questions (FAQ)

Q: Will buyers accept all owner compensation as an add-back?

A: No. Buyers rarely accept the full owner compensation as an add-back. They typically normalize it to a market-rate replacement salary for the functional role the owner performs (e.g., managing partner, rainmaker, or technical expert). The excess above that market rate can often be added back, but buyers require strong documentation such as salary surveys, role descriptions, and time studies to support the adjustment.

Q: When should I start preparing for a Quality of Earnings review?

A: Ideally 12 to 24 months before going to market. This gives you enough time to clean up financials, document add-backs, improve client retention, reduce owner dependency, modernize systems, and address any red flags. Starting early allows you to fix issues proactively rather than reacting during buyer due diligence, which can protect or even increase your valuation.

Q: What is the difference between a standard audit and a QoE report?

A: A standard audit verifies that your financial statements comply with GAAP for historical accuracy. A QoE report goes much further — it analyzes the sustainability of earnings, normalizes for non-recurring and owner-specific items, and evaluates risk factors important to buyers for future performance.

Q: Can a strong QoE report really increase my firm’s sale price?

A: Yes. A well-prepared sell-side QoE report can validate higher normalized EBITDA, reduce buyer skepticism, speed up due diligence, and support a higher multiple — often adding hundreds of thousands or even millions to the final purchase price.

Q: How important is revenue mix (engagement types and average fees) in the QoE process?

A: Extremely important. Buyers carefully analyze your mix of 1040s, 1065s, 1120s, 990s, CAS, advisory, and other services, along with average fees. A healthier mix with more recurring, higher-fee work generally leads to stronger multiples and better terms

Conclusion & Next Steps

Quality of Earnings (QoE) has become one of the most critical factors in successful CPA firm sales in 2026. For firms in the $750K–$5M revenue range, buyers are no longer satisfied with surface-level financials. They perform detailed analysis of revenue mix, engagement types, average fees, add-backs, working capital, operational strength, and succession readiness to determine the true sustainable value of your practice.

Firms that proactively manage their QoE story — through clean financials, strong documentation, balanced service mix, modern systems, and reduced owner dependency — consistently achieve higher multiples, better deal terms, and smoother transitions. On the other hand, overlooked weaknesses in these areas can lead to significant valuation discounts or lost opportunities.

The good news is that most of these factors are within your control. Starting preparation early (12–24 months in advance) gives you the best chance to strengthen your firm’s position and maximize your exit value.

Ready to Explore Your Options?

Contact Ashley-Kincaid today for a confidential, no-obligation assessment.

Our team specializes in working with serious CPA firm owners in the $750K–$5M revenue range. We provide clear, buyer-perspective insights to help you understand your firm’s true market value, identify opportunities to strengthen earnings quality, reduce risk, and navigate the entire sale process with confidence and maximum results.