Common Challenges and Smart Strategies for PE CPA Firm Sales in 2026

Ashley-Kincaid | July 2, 2026

Selling your CPA firm to a private equity buyer is a major milestone that represents the culmination of years of hard work, dedication, and building a valuable business. While the transaction and post-sale experience are exciting opportunities for liquidity and growth, many sellers later reflect on certain aspects they wish they had approached differently — from earn-out structures and post-sale roles to cultural integration and operational changes. These reflections often center on how small adjustments during preparation could have led to even better financial returns and a more satisfying transition.

Understanding the most common experiences — based on real insights from CPA firm owners who have successfully completed the process — and applying practical strategies can help you achieve a more successful, satisfying, and financially rewarding outcome. With the right preparation, expert guidance, and realistic expectations, you can navigate the sale and transition with greater confidence, maximize your upside, and look back on the experience with pride and accomplishment.

As specialists in CPA firm M&A with a proprietary database of over 60,000 firms and strategic relationships with PE and CPA firm buyers that are unique in the industry, Ashley-Kincaid has supported numerous transactions and seen firsthand what separates successful exits from those with lingering regrets.

Related: Understanding the Private Equity Fund Lifecycle: Why Strategic Timing Benefits CPA Firm Sellers

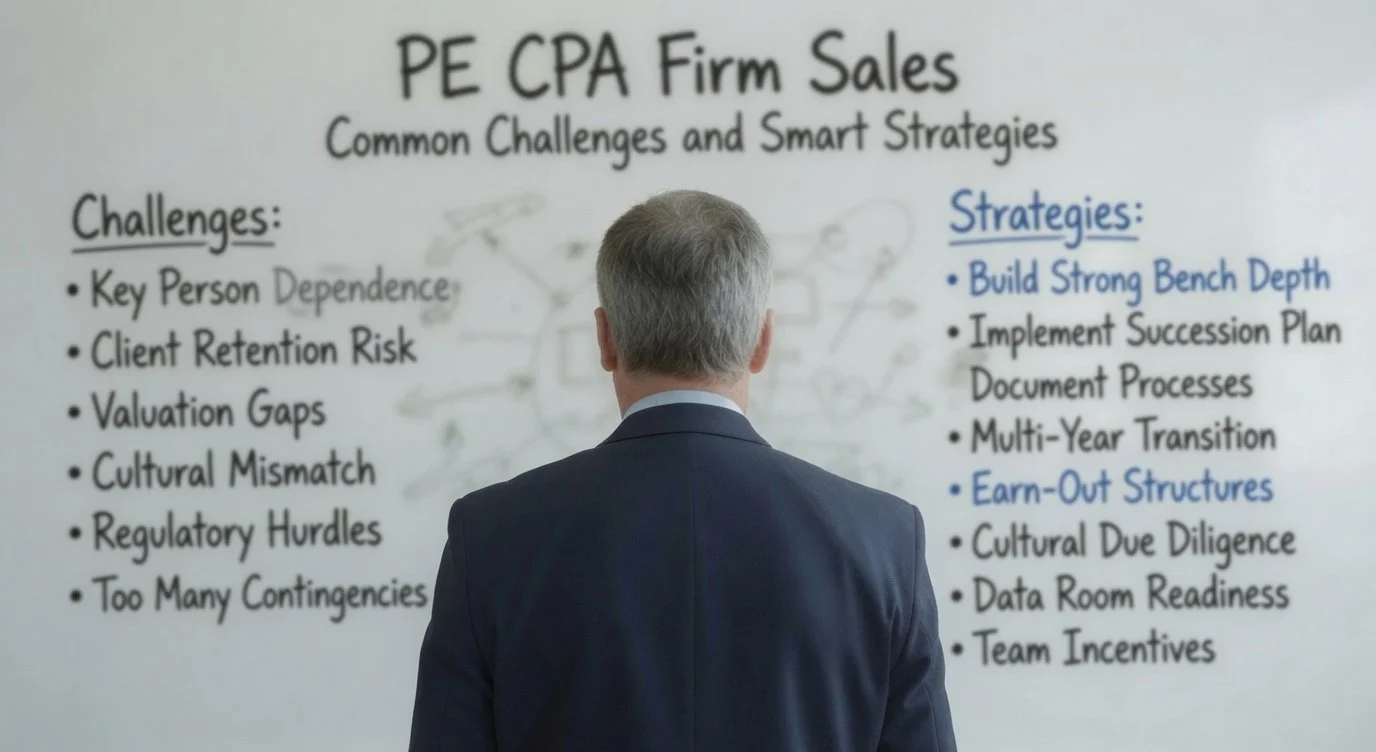

Common Regret 1: Accepting a Weak Deal Structure

Many sellers later wish they had negotiated stronger terms around earn-outs, cash at close, and rollover equity, particularly when feeling pressure to move quickly. These decisions are often made without fully exploring all options or modeling the long-term implications. With thoughtful preparation and the right guidance, you can avoid this common pitfall and structure a deal that better balances immediate liquidity with long-term upside, leading to greater satisfaction and financial success.

How to Avoid It: Model multiple structure scenarios early in the process using detailed financial projections. Negotiate clear, achievable earn-out metrics with strong protections against buyer actions that could negatively impact performance. Work with an experienced advisor to balance immediate liquidity with long-term upside potential. Ashley-Kincaid helps clients run comprehensive financial models and scenario analyses to ensure the structure aligns with their personal and financial goals, often resulting in significantly better overall outcomes. See our article on EBITDA multiples and market trends.

Common Regret 2: Underestimating Post-Sale Cultural and Operational Changes

Sellers often underestimate the shift from entrepreneurial control to a more corporate, metrics-driven environment. The move to standardized reporting, centralized decision-making, and performance KPIs can feel restrictive and lead to frustration during the transition period.

How to Avoid It: Visit other portfolio companies (with buyer permission) and ask detailed questions about day-to-day life post-sale. Negotiate clear role definitions, decision-making authority, and protection periods in the employment agreement. Prepare your team for the transition well in advance through communication and training. Ashley-Kincaid advises clients to have open conversations about culture and operations early, helping them set realistic expectations and negotiate terms that preserve key aspects of their preferred working style. See our pillar guide: How Private Equity and CPA Firm Buyers Evaluate Quality of Earnings (QoE) in 2026.

Common Regret 3: Insufficient Succession and Talent Planning

Many owners regret not building a stronger second-tier team before the sale, leading to higher post-sale pressure, difficulty meeting earn-out targets, or challenges during integration.

How to Avoid It: Start leadership development and documentation 12–24 months before marketing the firm. Implement retention incentives, equity grants, and clear career paths for key talent. Ashley-Kincaid’s succession planning frameworks have helped many clients reduce owner dependency, strengthen buyer confidence, and create a more resilient organization that supports both the sale and long-term success. See our article on succession readiness.

Common Regret 4: Poor Timing Relative to Fund Cycles

Sellers who rush into a sale during late fund stages often regret accepting compressed multiples, heavier earn-outs, and less favorable terms due to reduced buyer leverage.

How to Avoid It: Align your timeline with active deployment periods. Work with an advisor who tracks PE fund activity to identify optimal windows. Ashley-Kincaid provides real-time intelligence on fund cycles, helping clients time their process for maximum leverage and better economics. See our article on PE fund lifecycle and strategic timing.

Common Regret 5: Inadequate Preparation of Financials and Data Room

Last-minute scrambling during diligence often leads to valuation discounts, delays, or lost momentum as buyers discover issues that could have been addressed earlier.

How to Avoid It: Prepare a professional data room and detailed Normalized EBITDA workpapers well in advance. Conduct a mock due diligence to identify and fix issues early. Ashley-Kincaid’s preparation checklists and mock diligence sessions have helped many sellers avoid surprises and maintain strong negotiating positions throughout the process.

By learning from the experiences of others and preparing proactively with expert guidance, you can avoid common regrets and achieve a successful, satisfying exit.

Action Steps to Avoid Common Regrets

Start preparation 12–24 months before marketing.

Engage experienced M&A, legal, and tax advisors early.

Model multiple deal structures and scenarios.

Build strong succession and retention plans.

Maintain realistic expectations about post-sale life.

By learning from the experiences of others and preparing proactively, you can avoid common regrets and achieve a successful, satisfying exit.

Ready to Avoid Common Regrets and Maximize Your Exit?

Contact Ashley-Kincaid for a no-obligation consultation. As the leading specialists in CPA firm M&A, we’ll provide a custom regret-prevention assessment, tailored preparation roadmap, and expert guidance to help you achieve the best possible outcome.