How to Value My CPA Firm for Sale in 2026: Complete Guide with Multiples, Methods & Real Examples

Selling a CPA firm is one of the most significant financial decisions an owner will ever make. It represents years — often decades — of hard work building a valuable practice, serving clients, developing a strong team, and creating a legacy that supports your family and future goals.

For many owners, the sale of their firm is the primary vehicle for retirement funding, wealth transfer, or pursuing new opportunities. Understanding how the market currently values accounting firms in 2026 is therefore the critical first step toward maximizing your sale price, negotiating favorable terms, and achieving a smooth, successful transition.

Quick Answer: Most CPA firms sell between 0.9x and 1.3x annual gross revenue, with many transactions landing near 1.0x. Stronger firms with recurring revenue, clean financials, diversified clients, and a solid transition-ready team can command higher multiples. Larger firms (typically over $2M–$5M in revenue) are often valued primarily on EBITDA and typically sell for 3.5x – 4.5x on EBITDA. The final price also depends heavily on profitability, client mix, staff strength, location, deal structure (cash at close, earnouts, seller financing), and current market conditions.

1. Primary Valuation Methods for CPA Firms

Buyers typically use one or more of the following approaches:

Revenue Multiples (Most Common) The simplest and most widely used method. Buyers apply a multiple to your annual collected fees or gross revenue.

EBITDA / SDE Multiples Normalized earnings (Seller’s Discretionary Earnings or EBITDA) are especially important for more profitable or larger firms.

Hybrid / Adjusted Valuation Most real-world deals combine revenue and earnings approaches, then make specific adjustments.

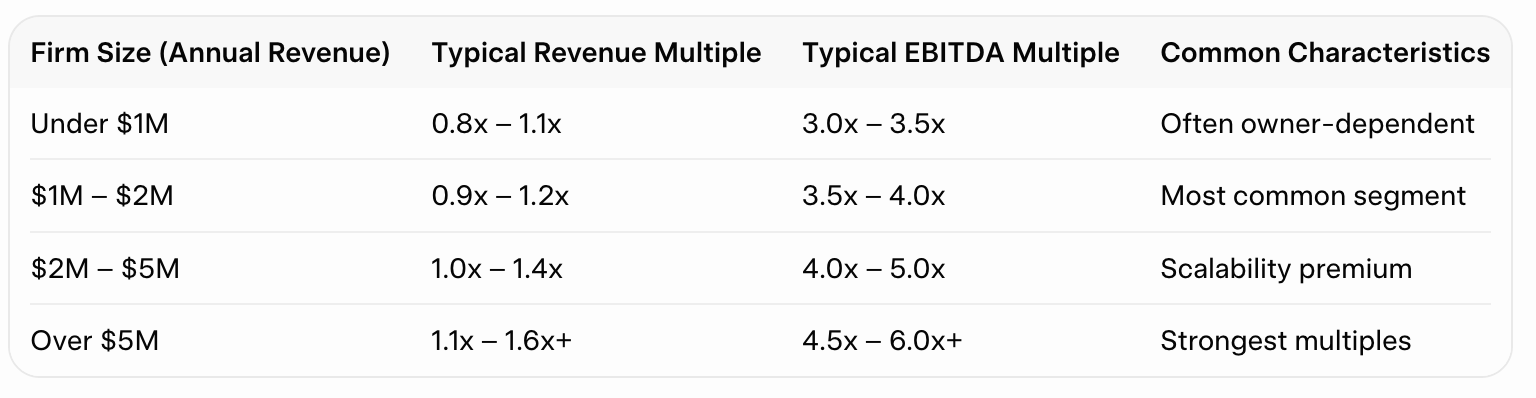

2. Current Market Multiples (2026)

From Ashley-Kincaid’s proprietary database and recent transactions:

Note: These are baseline figures. Actual multiples are adjusted based on the factors below.

3. Step-by-Step Practical Valuation Process

Calculate normalized annual gross revenue/collected fees (remove one-time items).

Apply a base market multiple based on firm size and performance.

Make specific adjustments for deal structure, client quality, profitability, and transition risk.

Example: A firm generating $800,000 in annual fees might have a preliminary valuation between $720,000 (0.9x) and $1,040,000 (1.3x) before final adjustments for payment terms and risk factors.

4. What Moves the Multiple Up or Down

Value-Enhancing Factors:

Recurring revenue and high client retention

Diversified client base

Desirable location or specialized niche

Clean financial records and above-average profitability

Owner willingness to support transition

Value-Reducing Factors:

Heavy dependence on the owner

Client concentration risk

Declining revenue or profitability trends

Outdated technology or weak processes

Partner/staff retention concerns

5. Special Situations

Tax Considerations should be carefully modeled with professional advice, as highlighted in publications from the American Institute of CPAs (AICPA).

Recent insights from the Journal of Accountancy also emphasize the importance of proper normalization and deal structuring in CPA firm sales.

6. Next Steps & Common Mistakes to Avoid

Preparation Checklist and avoiding common pitfalls like delaying planning are essential. For the latest industry trends, see reports from Accounting Today.

PitchBook industry reports further confirm that well-prepared firms continue to attract strong interest from private equity buyers.

Preparation Checklist:

Document client retention metrics

Update systems and processes

Prepare a professional information memorandum

Common Mistakes:

Relying solely on rule-of-thumb multiples

Delaying planning (start 12–24 months in advance)

Limiting buyer outreach to only one type (PE vs strategic)

FAQ

Q: What is a typical multiple for a CPA firm sale? A: Most transactions fall between 0.9x and 1.3x gross revenue, with adjustments based on the firm’s specific strengths and risks.

Q: Should valuation be based on revenue or EBITDA? A: Both are relevant. Revenue is the common starting point; EBITDA becomes more influential for highly profitable firms.

Q: How long does the sale process usually take? A: From preparation to closing, most deals take 6–12 months.

Considering a Sale in the Next 12-60 Months?

Take the Next Step — Confidentially

At Ashley-Kincaid, LLC, we specialize exclusively in CPA firm M&A. We offer no-obligation, confidential consultations. During this initial discussion we can:

Share relevant recent transaction comparables for firms similar to yours

Provide a realistic valuation range based on current 2026 market conditions

Outline what a professionally managed national buyer process would look like for your specific firm

Don’t leave meaningful value on the table by restricting your options to local buyers. Reach out today to explore what the national buyer market could mean for your future.