Understanding the Private Equity Fund Lifecycle: Why Strategic Timing Benefits CPA Firm Sellers

Private equity (PE) has become one of the most transformative forces in the accounting profession. With more than 50 PE-related transactions in the CPA sector in 2025 and sustained momentum into 2026, consolidation is fundamentally reshaping how firms think about ownership, growth, succession, and exit strategies. Nearly half of the top 30 largest U.S. CPA firms now have some form of private equity involvement. This shift is creating both opportunities and complexities for firm owners, particularly as traditional partnership models evolve toward institutional ownership.

For CPA firm owners considering a sale, succession, or liquidity event, understanding the private equity fund lifecycle is no longer optional — it is essential for making informed decisions that maximize value and optimize deal terms.

This comprehensive article provides an authoritative, detailed examination of the typical ~10-year PE fund lifecycle. It explores the economic incentives that drive General Partner (GP) behavior, the distinct phases of the cycle, why certain windows create meaningful advantages for sellers, platform versus add-on dynamics, valuation implications, risks, and actionable strategies tailored specifically to mid-sized CPA firms in the $3 million to $10 million+ revenue range.

1. The Structure and Economics of Private Equity Funds

Private equity funds are structured as closed-end limited partnerships. Limited Partners (LPs) — primarily institutional investors such as pension funds, university endowments, sovereign wealth funds, insurance companies, and high-net-worth family offices — commit capital to the fund. General Partners (GPs), the professional team at the PE firm, are responsible for sourcing, executing, managing, and exiting investments.

The compensation model is intentionally designed to align interests while providing GPs with both stability and high-upside potential:

Management Fees: Typically 1.5%–2% of committed capital annually during the investment period (stepping down later). These fees cover operations and provide predictable income.

Carried Interest: Usually 20% of profits after full return of capital and a preferred return hurdle (commonly 8%) to LPs. This is the primary wealth-creation mechanism for GPs.

This structure produces the classic “J-curve” return profile: early negative or flat returns due to fees and deployment costs, followed by strong gains during the harvest phase. Limited Partnership Agreements (LPAs) govern all terms, including investment periods, fee schedules, distribution waterfalls, clawbacks, and governance.

In 2025–2026, LPs have been selective, demanding clear theses in sectors like professional services and evidence of disciplined capital deployment. This selectivity heightens GP pressure during the investment period.

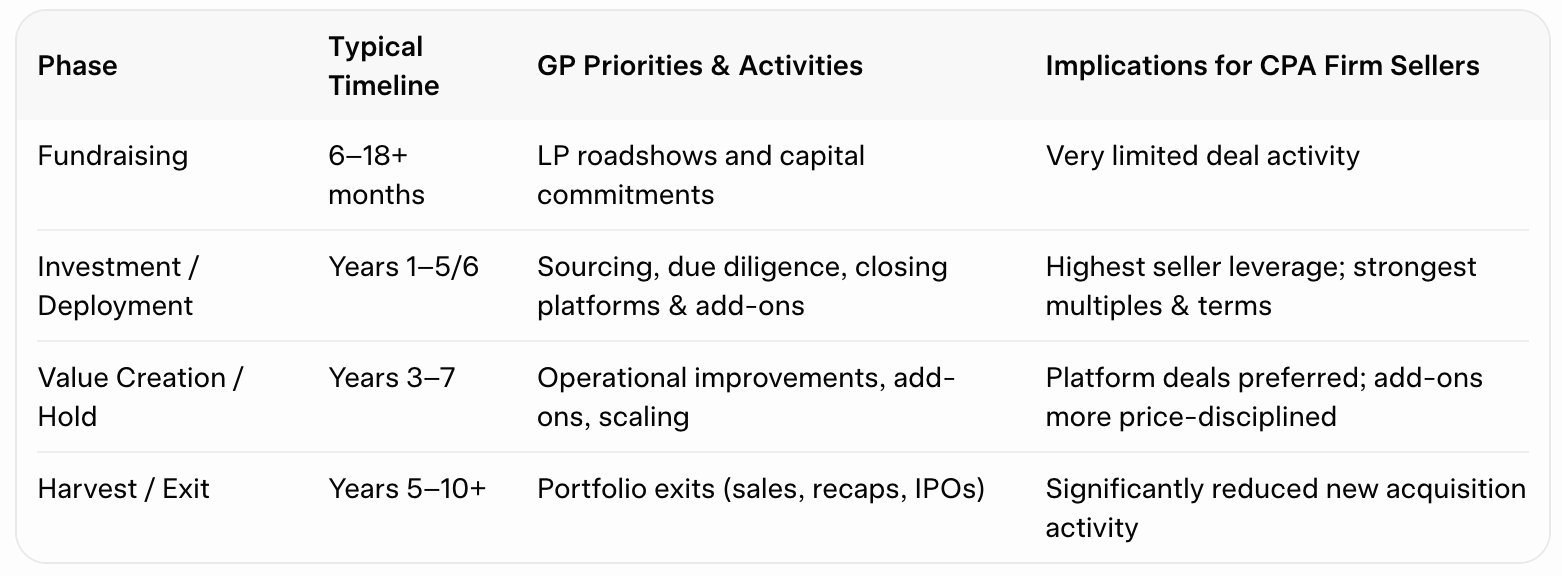

2. Detailed Phases of the ~10-Year Fund Lifecycle

The fund lifecycle generally unfolds across four overlapping phases:

Fundraising Phase: GPs focus on raising the fund by showcasing prior performance. Success here determines available dry powder.

Investment / Deployment Period: This is the most critical phase for sellers. GPs must deploy committed capital efficiently to demonstrate momentum and build a strong vintage year. Pressure is especially high when preparing for the next fundraise (typically years 3–6).

Value Creation / Hold Period: Emphasis shifts to growing portfolio companies through technology investments, talent upgrades, service expansion, and add-on acquisitions.

Harvest / Exit Phase: GPs focus on realizing gains. Extended hold periods (averaging over 6.5 years) are common in the current market.

3. Why Strategic Timing Benefits CPA Firm Sellers

The early-to-mid deployment period, particularly when a fund is approaching its next raise, creates the strongest seller advantages. GPs face pressure to deploy capital, demonstrate activity to LPs, and build a track record for successor funds. This often translates to more aggressive pursuit of quality assets and willingness to pay toward the higher end of the 3.5–4.5x adjusted EBITDA range.

Valuation Impact Modeling for a $4M Revenue Firm

Timing can easily represent a difference of $500,000 to over $1 million in seller proceeds for a mid-sized firm.

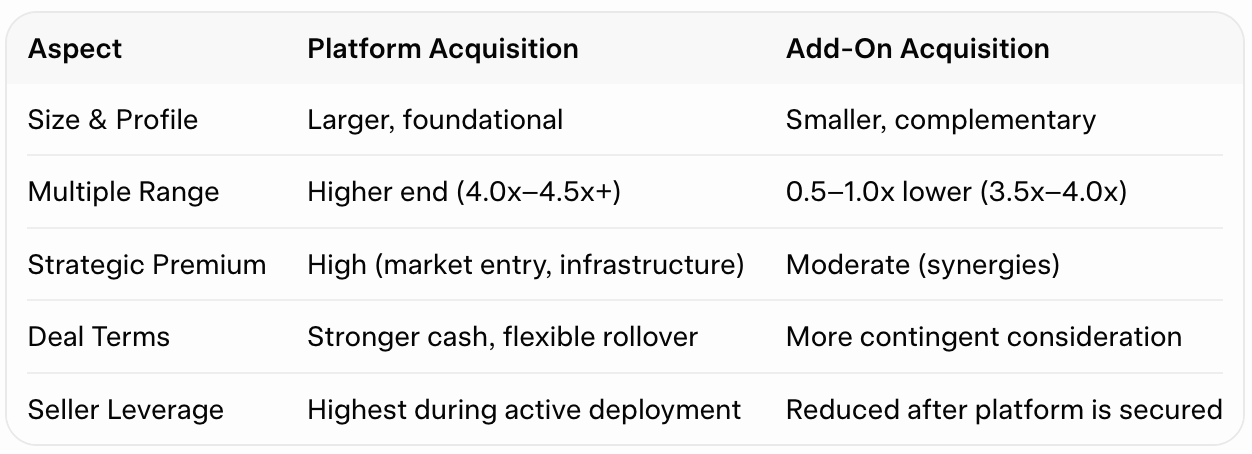

4. Platform vs. Add-On Dynamics in CPA Firm M&A

PE firms in professional services heavily favor buy-and-build strategies. A platform acquisition serves as the foundational anchor, justifying higher multiples due to its strategic importance. An add-on (tuck-in or bolt-on) is a complementary acquisition that benefits from the platform’s infrastructure.

Platform vs. Add-On Comparison

Platform Illustration Recent PE discussions have highlighted interest in strong CPA firms with approximately $4 million in revenue as potential platforms. Such an anchor provides immediate scale in the Southwest market, strong tax and advisory capabilities, and a foundation for regional or national expansion. Sellers who position their firms as strategic complements before these platform deals close can often command platform-like economics. Once the anchor is established, subsequent acquisitions shift to add-on treatment, resulting in more disciplined pricing and greater use of earn-outs.

5. Risks, Challenges, and 2026 Market Context

While the private equity fund lifecycle creates attractive windows for CPA firm sellers, it is essential to balance timing advantages with a clear understanding of the associated risks, operational challenges, and current market realities in 2026.

EBITDA Normalization Best Practices

Adjusted EBITDA is the cornerstone of valuation. PE buyers and their advisors perform rigorous scrutiny of financial statements. Key normalization areas for CPA firms include owner compensation (adding back amounts above fair-market replacement cost), non-recurring expenses, rent adjustments when real estate is personally owned, partner perks, and run-rate projections based on sustainable client retention. Firms that maintain detailed, well-documented workpapers for all adjustments typically achieve higher accepted EBITDA figures and experience smoother due diligence.

Deal Structuring Considerations

Headline multiples tell only part of the story. Critical elements include:

Cash at close (typically 40–70%, higher in strong deployment windows)

Rollover equity (usually 20–40%)

Earn-outs and performance-based payments

Seller notes

Sophisticated sellers model multiple scenarios, prioritizing total after-tax proceeds and risk allocation rather than focusing solely on the multiple.

Interest Rate Sensitivity

Although interest rates moderated in late 2025, borrowing costs remain elevated compared to previous years. Higher financing costs make PE firms more disciplined on entry multiples and more dependent on operational improvements and multiple arbitrage to generate returns. In this environment, high-quality firms with strong recurring revenue and clean financials continue to command attention, while higher-risk practices face greater scrutiny.

Regulatory Environment in Accounting

PE ownership of CPA firms operates under Alternative Practice Structures (APS) in most states, where PE entities can own non-attest operations while licensed CPAs retain control of attest services. Compliance remains complex, with ongoing focus from state boards on independence, fee-sharing, and quality control. Buyers in 2026 place significant emphasis on regulatory readiness, as any compliance gaps can delay closings or reduce post-deal value.

Post-Deal Realities

Many sellers underestimate the changes that follow closing:

Multi-year earn-out periods with continued operational involvement

Shift from partnership culture to professional, KPI-driven management

Increased reporting requirements and reduced autonomy

Need for sophisticated personal wealth and tax planning after liquidity

Clear expectations and carefully negotiated employment and shareholder agreements are critical for long-term success.

2026 Market Outlook

The CPA firm M&A market remains constructive for well-prepared sellers. Deployment pressures and pre-fundraise activity continue to support competitive interest, particularly for firms with strong recurring revenue, advisory services, and professionalized operations. Geographic hot spots such as Arizona, Nevada, Texas, and Florida are seeing elevated platform-building activity. However, buyer selectivity has increased — quality, strategic fit, and execution readiness are rewarded, while weaker opportunities face more disciplined pricing.

By proactively addressing normalization, structuring, regulatory, and post-deal considerations, CPA firm owners can convert theoretical timing advantages into successful, value-maximizing transactions.

6. Strategic Recommendations and Comprehensive Implementation Framework

To capitalize on favorable windows in the PE fund lifecycle, CPA firm owners should follow a structured preparation approach. The following framework helps maximize valuation and negotiation leverage.

12–24 Month Preparation Timeline

Months 12–18: Focus on financial cleanliness — normalize EBITDA, document add-backs, and strengthen recurring revenue.

Months 6–12: Build operational scalability through technology upgrades, second-tier leadership development, and client retention systems.

Months 1–6: Prepare marketing materials, run a confidential market assessment, and align personal and firm goals.

Key Strategies to Enhance Positioning

Increase the percentage of recurring and advisory revenue.

Reduce key-person dependency through documented processes and strong management depth.

Demonstrate geographic or service-line synergies that complement active PE platforms.

Maintain clean, audit-ready financials with detailed normalization workpapers.

Essential Questions to Ask Potential Buyers

Where is your current fund in its deployment cycle and when do you expect to raise the next fund?

Will our firm be viewed as a platform or an add-on?

What are your typical cash-at-close percentages and rollover equity expectations?

How do you support post-deal integration and growth?

Negotiation Frameworks

Prioritize total after-tax proceeds over headline multiples. Negotiate for higher cash at close, protective governance rights on rollover equity, realistic earn-out targets, and clear definitions of EBITDA calculations. Engage experienced counsel early to review LOIs and transaction documents.

By following this framework, CPA firm owners can transform theoretical timing advantages into concrete results — stronger multiples, better terms, and a smoother transaction process.

Conclusion

The private equity fund lifecycle offers a predictable framework for opportunity. By understanding deployment pressures, pre-fundraise dynamics, and platform strategies, CPA firm owners can significantly improve their valuation and deal outcomes.

Considering a Sale in the Next 12-60 Months?

Take the Next Step — Confidentially

At Ashley-Kincaid, LLC, we specialize exclusively in CPA firm M&A. We offer no-obligation, confidential consultations. During this initial discussion we can:

Share relevant recent transaction comparables for firms similar to yours

Provide a realistic valuation range based on current 2026 market conditions

Outline what a professionally managed national buyer process would look like for your specific firm

Don’t leave meaningful value on the table by restricting your options to local buyers. Reach out today to explore what the national buyer market could mean for your future.