CPA Firm Valuation: A Conservative LBO Approach – Part 1: Inputs & Normalized EBITDA

Introduction

In the competitive landscape of professional services, valuing a Certified Public Accountant (CPA) firm requires a meticulous blend of financial analysis, industry insight, and conservative forecasting. For potential buyers considering a Leveraged Buyout (LBO), determining the maximum willingness to pay hinges on a realistic assessment of the firm's earning potential. This series of articles, brought to you by Ashley-Kincaid, explores key components of CPA firm valuation through a conservative LBO lens. We will draft six focused articles, each delving into a distinct topic to build a comprehensive framework for buyers and sellers alike.

Our first installment centers on Inputs & Normalized EBITDA, a foundational step in the valuation process. Normalized EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) adjusts reported financials to reflect the true, sustainable earning power of the business under new ownership. This normalization is crucial for CPA firms, where owner discretionary expenses, one-time items, and non-recurring revenues can distort the picture. By starting with raw inputs and methodically adjusting them, we arrive at a "Normalized Entry EBITDA" – the entry-level earnings metric used to project future cash flows in an LBO model.

This article will guide you through the process step by step, using a standardized template format commonly employed in due diligence. We'll explain each line item, the rationale for adjustments, and how to compute the implied margins. Whether you're a private equity investor, a strategic buyer, or a CPA firm owner preparing for sale, understanding this process ensures a conservative, defensible valuation.

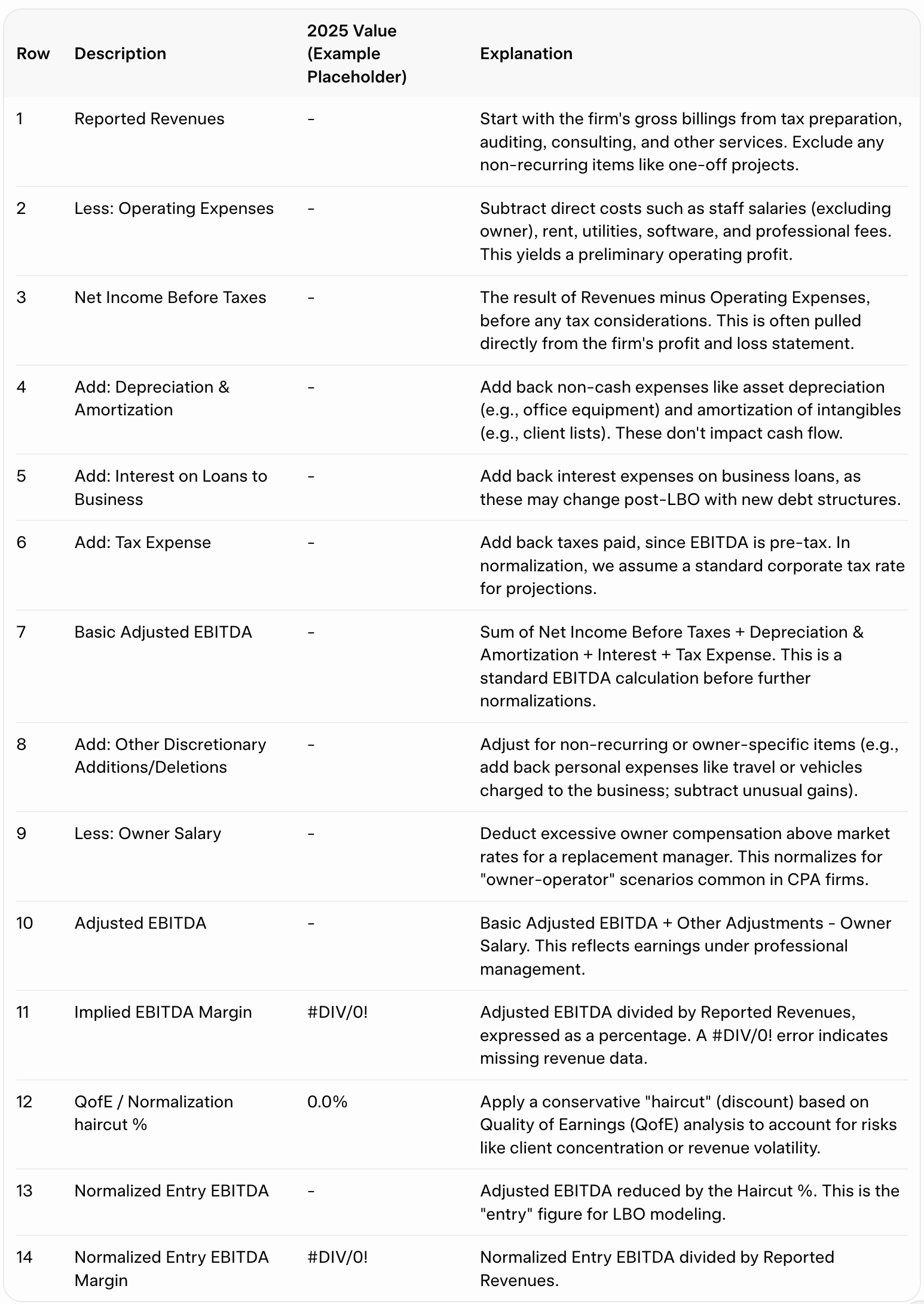

Understanding the Template: Section 1 – Inputs & Normalized EBITDA

The template provided is a structured worksheet for a single projection year (e.g., 2025), but in practice, this would be extended across a multi-year forecast. It begins with reported financials and applies adjustments to derive a normalized figure. Here's the breakdown with rows renumbered sequentially starting at 1:

This template ensures transparency and conservatism, aligning with LBO principles where over-optimism can lead to unsustainable debt loads.

Step-by-Step Guide to Calculating Normalized Entry EBITDA and Margin

To derive a Normalized Entry EBITDA and its margin, follow this systematic approach. We'll use hypothetical numbers for a mid-sized CPA firm to illustrate (assume all figures in USD thousands for 2025 projections).

Step 1: Gather and Input Raw Financial Data

Reported Revenues (Row 1): Begin with audited or management-provided revenues. For a CPA firm, this might include $2,500 from recurring tax and audit services. Exclude any windfalls, like a one-time M&A advisory fee.

Operating Expenses (Row 2): Input $1,800, covering staff wages ($1,000), office costs ($300), marketing ($200), and other overhead ($300). Ensure these are normalized – e.g., adjust for inflated costs due to owner perks.

Net Income Before Taxes (Row 3): Automatically calculates as Revenues - Expenses = $700.

Tip: Source data from the firm's trailing twelve months (TTM) financials, adjusted for seasonality (e.g., tax season peaks).

Step 2: Add Back Non-Cash and Financing Items

Depreciation & Amortization (Row 4): Add $150 for office tech and software amortization. This is non-cash, so it boosts EBITDA.

Interest on Loans (Row 5): Add $50 for existing business debt interest.

Tax Expense (Row 6): Add $200, representing taxes on pre-tax income.

Basic Adjusted EBITDA (Row 7): $700 (Net Income) + $150 (D&A) + $50 (Interest) + $200 (Taxes) = $1,100.

Rationale: These add-backs standardize the metric, focusing on operational cash generation independent of capital structure or tax strategy.

Step 3: Apply Discretionary and Ownership Adjustments

Other Discretionary Additions/Deletions (Row 8): Add back $100 for owner personal expenses (e.g., family health insurance or non-business travel) and subtract $50 for a non-recurring grant. Net: +$50.

Owner Salary (Row 9): If the owner draws $300 but a market-rate CEO salary is $150, subtract the excess $150 to normalize.

Adjusted EBITDA (Row 10): $1,100 + $50 - $150 = $1,000.

Key Insight for CPA Firms: Owners often blend personal and business expenses. A thorough QofE review (e.g., by engaging forensic accountants) identifies these. Conservatism dictates erring on the side of higher deductions for owner comp if market data suggests it.

Step 4: Compute Implied Margin and Apply Haircut

Implied EBITDA Margin (Row 11): $1,000 / $2,500 = 40%. This benchmark should align with industry averages (CPA firms often range 25-45%, per benchmarks from sources like the AICPA or Sageworks).

QofE / Normalization Haircut % (Row 12): Apply a 10% discount for risks like key client dependency (e.g., 20% of revenue from one client) or economic sensitivity. Conservative LBOs often use 5-20% haircuts.

Normalized Entry EBITDA (Row 13): $1,000 * (1 - 10%) = $900.

Normalized Entry EBITDA Margin (Row 14): $900 / $2,500 = 36%.

Conservative Considerations: The haircut ensures the EBITDA is "entry-level" – sustainable from Day 1 post-acquisition. For CPA firms, factor in client retention risks (e.g., 10-20% attrition post-sale) or regulatory changes (e.g., tax code shifts).

Why Normalization Matters in CPA Firm LBOs

In a conservative LBO, Normalized Entry EBITDA forms the basis for debt capacity calculations. Lenders typically allow 3-5x EBITDA leverage for CPA firms due to stable cash flows. Overstating EBITDA risks default; understating it leaves value on the table. For example, with $900 Normalized EBITDA at a 4x multiple, max debt might be $3,600, influencing your willingness to pay.

Conclusion

Mastering Inputs & Normalized EBITDA sets the stage for a robust CPA firm valuation. By methodically adjusting from reported figures to a haircut-applied entry metric, you ensure conservatism in your LBO model. In our next article, we'll explore Multiples & Valuation Ranges, building on this foundation to determine enterprise value.

For personalized valuation services or to discuss your CPA firm's LBO potential, contact Ashley-Kincaid at our Las Vegas office. Stay tuned for Parts 2-6 in this series!

Ready to explore what your CPA firm is truly worth in today's market?

Whether you're considering a full exit, a partial sale, or simply want a no-obligation valuation benchmark to understand your options, Ashley-Kincaid specializes in helping CPA firm owners maximize value while protecting their legacy and team.

Schedule a confidential, 30-minute discovery call with our team today. We'll review your firm's key metrics, discuss current market multiples for CPA practices, and outline realistic paths forward—all at no cost and with complete discretion.

👉 Schedule Your Free Valuation Discovery Call Now

Don't leave money on the table or miss the right timing in this active M&A environment for accounting firms. Let's talk about your future—your schedule, your terms.

We look forward to connecting soon!