How Buyer Due Diligence on Revenue Mix Affects CPA Firm Valuations in 2026

Ashley-Kincaid | July 6, 2026

When private equity platforms and strategic acquirers evaluate a CPA firm, one of the first and most important deep dives they perform is into the firm’s revenue mix. This analysis goes far beyond simply looking at total revenue — it is a cornerstone of the Quality of Earnings (QoE) review and often has a greater impact on the final valuation than many owners realize.

In today’s market, buyers are not just purchasing historical financial performance. They are buying future cash flow potential. Revenue mix reveals how predictable, scalable, and transferable that cash flow is likely to be after the current owner transitions out. A well-balanced revenue mix with strong recurring services and healthy average fees signals lower risk and higher value. Conversely, heavy concentration in seasonal, low-fee, or owner-dependent work raises concerns about post-sale performance and typically results in more conservative multiples.

This level of scrutiny is particularly relevant for firms in the $750K–$5M revenue range, where buyers must underwrite the acquisition carefully to ensure debt service and return targets can be met. Understanding how buyers dissect revenue mix during due diligence is therefore essential for any serious seller.

As detailed in our main pillar guide, “How Private Equity and CPA Firm Buyers Evaluate Quality of Earnings (QoE) in 2026”, buyers are looking beyond total revenue to understand the quality, predictability, and transferability of that revenue after the sale.

Why Revenue Mix Matters So Much in 2026

In a competitive M&A market, buyers are under pressure to acquire practices with stable, scalable cash flows. Revenue mix directly affects their confidence in future performance. A firm with a strong mix of recurring, higher-margin services will generally command a higher EBITDA multiple than one heavily reliant on seasonal or low-fee work.

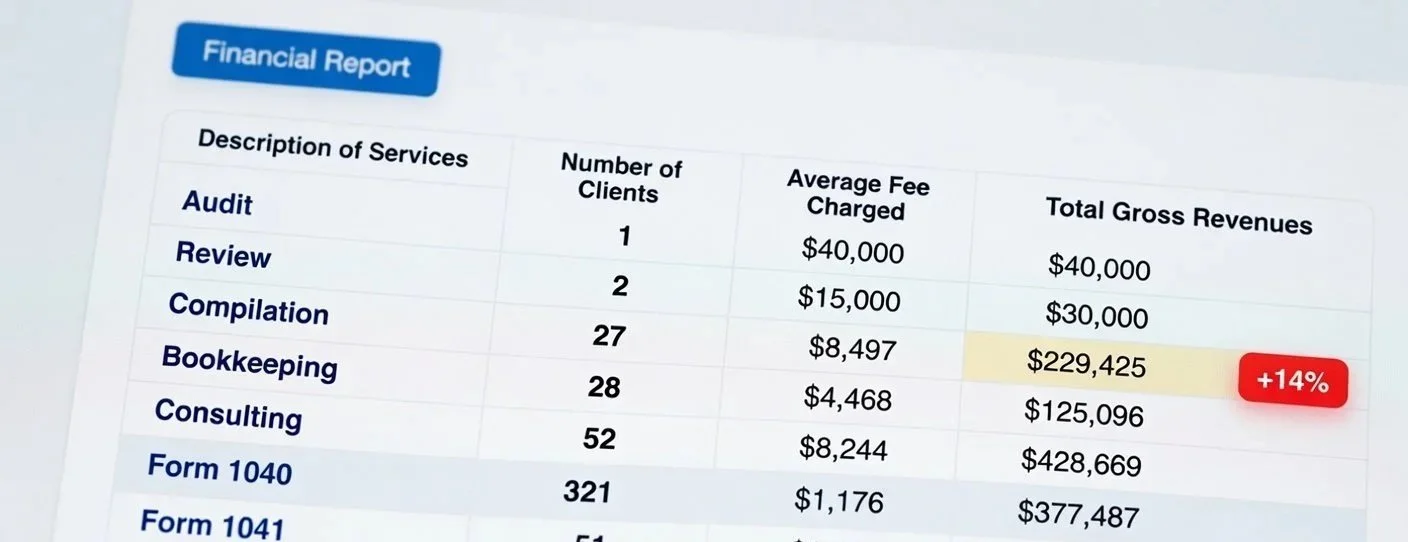

Key components buyers analyze include:

Percentage of recurring vs. project-based revenue — Buyers strongly prefer predictable, month-to-month or annual recurring streams over one-time or project work.

Breakdown by engagement type (1040s, 1120/1120S, 1065s, 990s, CAS, advisory, audits, and other services) — They evaluate the balance and quality of each service line.

Average fees per engagement or per client — Higher average fees signal stronger pricing power, better client relationships, and higher profitability.

Seasonality patterns and cash flow consistency — Significant tax-season spikes versus stable year-round revenue is closely scrutinized.

Client retention and tenure by service line — How sticky clients are within each engagement type.

Realization rates — The percentage of billed fees actually collected, which indicates billing efficiency and client satisfaction.

Revenue concentration by client or service line — Over-reliance on a small number of clients or service types raises risk flags.

Historical fee growth and pricing power — Evidence that the firm can successfully increase fees over time.

How Different Engagement Types Influence Valuation

High-Value Recurring Services (CAS, Bookkeeping, Outsourced CFO, Advisory)

These are considered the gold standard by most buyers in 2026. Services like Client Accounting Services (CAS), monthly bookkeeping, outsourced CFO work, and ongoing advisory retainers typically deliver higher average fees, stronger profit margins, and highly predictable monthly or quarterly revenue. Because they are recurring and less seasonal, they reduce buyer risk and improve cash flow visibility.

Firms with 50% or more of revenue coming from these high-value recurring services often receive meaningful positive adjustments to their EBITDA multiple — frequently in the range of +0.4x to +0.9x. Buyers view these practices as more scalable and easier to integrate into larger platforms.

Tax Compliance Work (1040s, 1120/1120S, 1065s, 990s)

Tax compliance engagements make up a large portion of many CPA firms, but they are evaluated differently depending on complexity:

Individual Tax Returns (1040s) are often viewed as lower quality due to strong seasonality, commoditization, and relatively lower average fees. Heavy reliance on 1040s can lead to negative multiple adjustments (typically -0.2x to -0.4x).

Corporate (1120/1120S), Partnership (1065), and Non-Profit (990) returns generally score better, especially when they involve complex planning, multi-state issues, or advisory components. These engagements tend to have higher average fees and better margins, resulting in neutral to modestly positive treatment.

One-Time and Project Work

This category is the least favored by buyers. One-time projects, special consulting assignments, and non-recurring work are difficult to predict and transfer to new owners. Because they lack repeatability, buyers apply the heaviest discounts here — often -0.4x to -0.8x or more — and may significantly reduce the weight given to this revenue when calculating normalized EBITDA.

Real-World Valuation Impact

To illustrate the importance of revenue mix, consider two similar CPA firms, each generating $2.8 million in annual revenue:

Firm A has a strong, modern service mix with 58% coming from recurring CAS, bookkeeping, outsourced CFO, and advisory work at solid average fees. During the Quality of Earnings review, buyers see high predictability, lower seasonality risk, and better transferability. As a result, they apply a 4.0x normalized EBITDA multiple.

Firm B generates a similar total revenue but with 68% coming from seasonal individual tax returns (1040s) and basic compliance work at lower average fees. Buyers perceive higher risk due to strong seasonality, client attrition potential, and limited scalability. They apply a more conservative 3.0x multiple.

The financial difference is substantial. Assuming similar normalized EBITDA after adjustments, the gap between a 4.0x and 3.0x multiple can easily exceed $1 million in enterprise value — sometimes significantly more depending on the final adjusted earnings figure.

This example demonstrates why revenue mix is one of the first areas sophisticated buyers examine closely during due diligence. A favorable mix can be worth hundreds of thousands — or even millions — at closing.

What Buyers Want to See in Revenue Mix

Sophisticated buyers look for clear evidence of a healthy, sustainable revenue foundation. The strongest firms demonstrate the following characteristics during QoE due diligence:

Recurring revenue trending upward — Buyers favor firms that are intentionally shifting toward more predictable, month-to-month or quarterly revenue streams. A clear upward trend in the percentage of recurring revenue over the past 3 years is highly valued.

Average fees that demonstrate pricing power — Higher average fees per client or per engagement signal strong client relationships, specialized expertise, and the ability to command premium pricing. Buyers review fee trends over time to assess whether the firm has successfully increased rates without significant client loss.

Diversification across engagement types — A balanced portfolio that includes a healthy mix of CAS, advisory, complex tax work (1065s, 1120s, 990s), and audits is preferred over heavy concentration in any single category, especially low-fee seasonal 1040s.

Evidence of client stickiness and low attrition — Strong historical retention rates, long client tenure, and documented client transition processes give buyers confidence that revenue will remain stable after the sale.

Firms that can clearly document these strengths — through detailed schedules, retention reports, fee analyses, and client feedback — are much better positioned to defend higher normalized EBITDA and secure stronger multiples during negotiations.

Actionable Steps to Strengthen Your Revenue Mix

Gradually shift capacity toward higher-value CAS and advisory services

Implement strategic fee increases on underpriced engagements

Document client retention trends and transition processes

Reduce reliance on low-fee seasonal work where possible

Conclusion

Revenue mix is not just a line item — it is one of the strongest predictors of the multiple you will receive. By understanding how buyers evaluate this during Quality of Earnings due diligence, you can make informed decisions that strengthen your firm’s position and maximize your exit value.

Ready to Evaluate Your Firm’s Revenue Mix and Overall QoE Strength?

Contact Ashley-Kincaid today for a confidential strategic QoE assessment tailored specifically for CPA firms in the $750K–$5M revenue range.

Our team provides clear, buyer-perspective insights to help serious sellers understand their current market position, strengthen earnings quality, reduce risk, and maximize their exit value in today’s competitive environment.